Conventional vs. Halal Mortgages: Choosing the Right Path to Home Ownership

Purchasing a home is an exciting milestone for many families and individuals. Choosing the right financial path to home ownership is just as important as choosing the home itself. Personal values, such as religious ideologies, impact an individual’s decision when purchasing a home.

For example, paying interest on a loan is not permissible in Sharia law. This places many practicing Muslims in the difficult position of choosing between their faith and home ownership.

Fortunately, lenders are now introducing halal mortgages that are an alternative financing model to the conventional interest-based mortgage, which removes that barrier to home ownership.

Halal mortgages are available to anyone in Alberta and this article explores the key differences between conventional mortgages and halal mortgages, which will allow buyers to better understand their options.

What Is a Conventional Mortgage?

A conventional mortgage is the standard method to finance the purchase of a home in Alberta. In this arrangement, a bank or other financial institution lends money to the buyer, who uses those funds to pay the seller. To secure its interest in repayment, the financial institution registers a mortgage against the home’s title at the Alberta Land Titles Office.

The buyer repays the loan over a set period through regular monthly payments that includes:

Principal: the amount borrowed; and

Interest: the cost of borrowing the money.

Risks of a Conventional Mortgage

Conventional mortgages carry several risks, many of which are tied to interest rates and long‑term financial uncertainty.

Variable‑rate mortgages expose borrowers to fluctuating payments. If interest rates rise, monthly payments can increase unexpectedly, particularly during periods of economic instability.

Fixed‑rate mortgages may feel more predictable in the short term, but borrowers are not immune to interest rate risk. Upon renewal, the mortgage may convert to a higher rate, resulting in increased monthly payments and overall borrowing costs.

For buyers seeking alternatives to interest‑based financing, halal mortgages offer a distinct approach.

What is a Halal Mortgage?

Halal mortgages are alternative financing models designed to allow buyers to comply with Islamic principles. Under Sharia law, the charging or paying of interest is prohibited, making conventional mortgages incompatible for many Muslims. While halal mortgages were designed with the Islamic faith in mind, they are open to any Albertan who wishes to forgo the economic uncertainty of a conventional mortgage. Halal mortgage arrangements are fully documented and registered at the Alberta Land Titles Office, ensuring they are legally recognized and enforceable.

How Halal Mortgages Work

Rather than charging interest, a halal mortgage changes the legal relationship between the parties. There are three common models:

1. Ijara (Lease‑to‑Own)

In an Ijara arrangement, the financier purchases the home and leases it to the buyer. The buyer occupies the property and makes regular payments, and ownership transfers to the buyer at the end of the lease term.

2. Musharakah (Diminishing Partnership)

In a Musharakah model, the buyer and the financier jointly purchase the home. The buyer lives in the home and makes monthly payments consisting of:

Rent for the financier’s ownership share; and

Payments that gradually buy out the financier’s interest.

Over time, the buyer becomes the sole owner of the property.

3. Murabaha (Cost Plus Profit Sale)

In a Murabaha transaction, the financier purchases the home and initially owns it. The financier then sells the home to the buyer at a price that includes the original purchase cost plus an agreed‑upon profit. The buyer pays this total amount in fixed, predictable installments, often over an amortization period of 25 years.

In Alberta, financiers use the Murabaha arrangement, so buyers can now apply for a halal mortgage utilizing the cost plus profit approach.

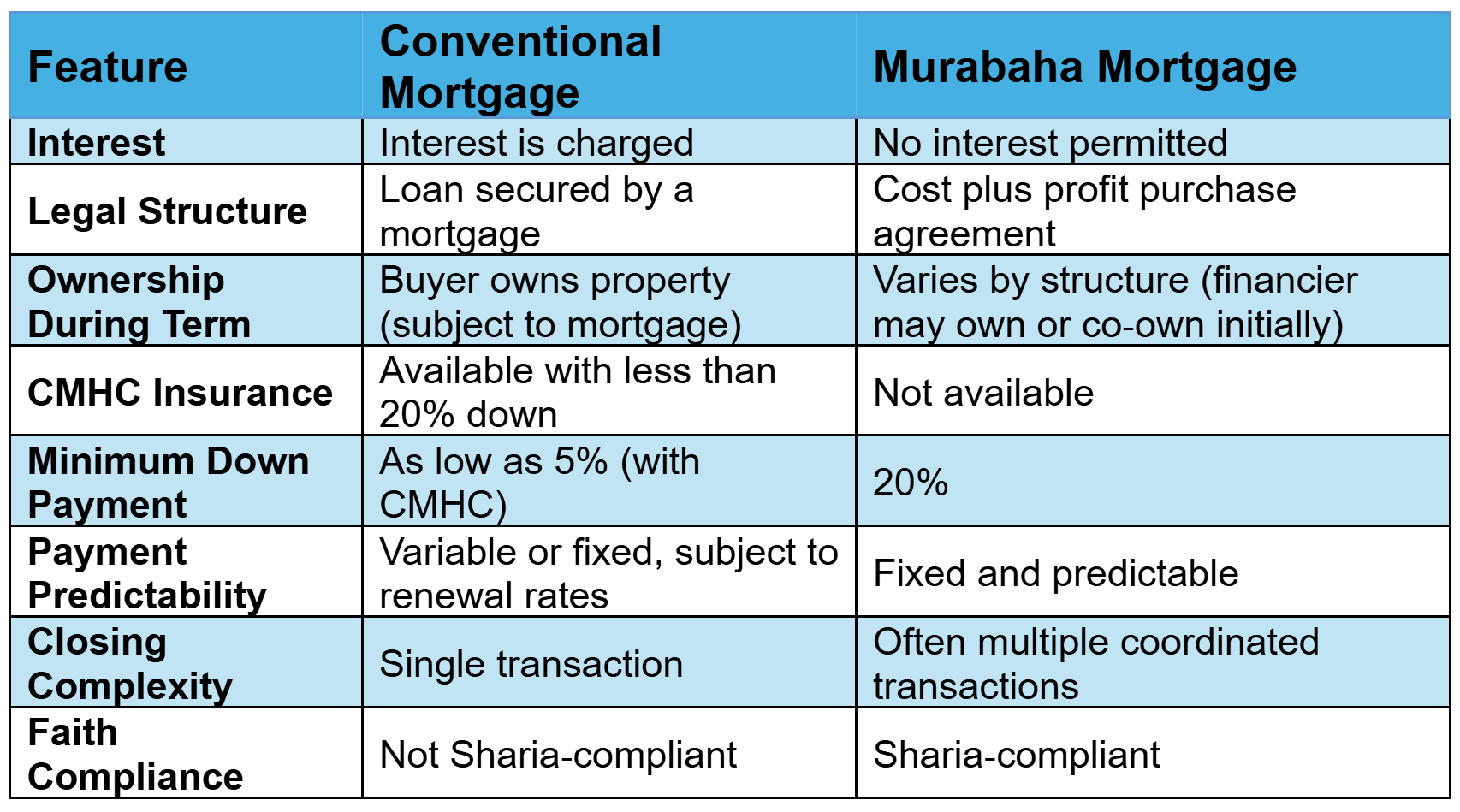

Key Differences at a Glance

Considerations When Choosing a Halal (Murabaha) Mortgage

The Canada Mortgage and Housing Corporation (CMHC) provides default insurance for loans. Halal mortgages do not qualify for CMHC insurance and therefore a buyer using a halal mortgage to purchase a property must have a minimum 20% down payment.

Higher Overall Cost

While halal mortgages offer long‑term payment certainty, they may ultimately cost more than a conventional mortgage if interest rates remain low over time.

Closing Procedures and Timing

Murabaha arrangements have unique closing requirements:

Closings occur only on the first of the month.

A Murabaha transaction involves two sequential closings:

The lender purchases the property from the seller; and

The buyer purchases the property from the lender.

Both transactions must typically be completed before noon, as required by Alberta conveyancing practice and Land Titles procedures.

The lender’s purchase must be finalized before the Murabaha agreement can be signed. The timing of these transactions must be performed with precision to ensure compliance with Alberta Land Titles.

Why Experienced Legal Advice Matters

Halal mortgage arrangements involve additional legal, procedural, and compliance requirements, including adherence to certification standards set by the Canadian Islamic Finance Board.

At SB LLP, our team includes experienced solicitors and conveyancers with in‑depth knowledge in conducting Murabaha transactions. While Murabaha arrangements involve more steps than a conventional mortgage, we are here to guide you through the process from start to finish. If you believe a halal mortgage best suits your home ownership needs, contact us early in the process so your transaction can be handled with care, clarity, and confidence.